Practical resources on the rules nonprofits operate under. Governance and fiduciary duties. Tax-exempt status and public-support tests. Lobbying and advocacy rules. Employment and volunteer compliance. Fiscal sponsorship.

Written for executive directors, board members, and senior leadership who want to understand the frameworks shaping their work.

The Nonprofit Law Primer.

The Other Lobbying Rules: State Registration and Reporting Requirements for Nonprofits

Federal 501(h) election covers your IRS exposure, but every state has its own lobbying registration regime, and once your advocacy crosses the state-defined threshold, missing the registration is a strict-liability problem that can shut a campaign down.

The Lobbying Rules Nonprofits Get Wrong — and the Power They're Leaving on the Table

Most 501(c)(3) leaders avoid lobbying entirely because they think the rules are restrictive, but the 501(h) election actually quantifies what's allowed, and the limits are higher than most boards realize, leaving real influence on the table.

What Nonprofit Employers Owe Their Employees Under Federal and State Law

Nonprofit status doesn't exempt you from federal or state employment law, which means your wage-and-hour exposure, benefits obligations, and discrimination liabilities are the same as any for-profit employer's, even when you can't pay market rates.

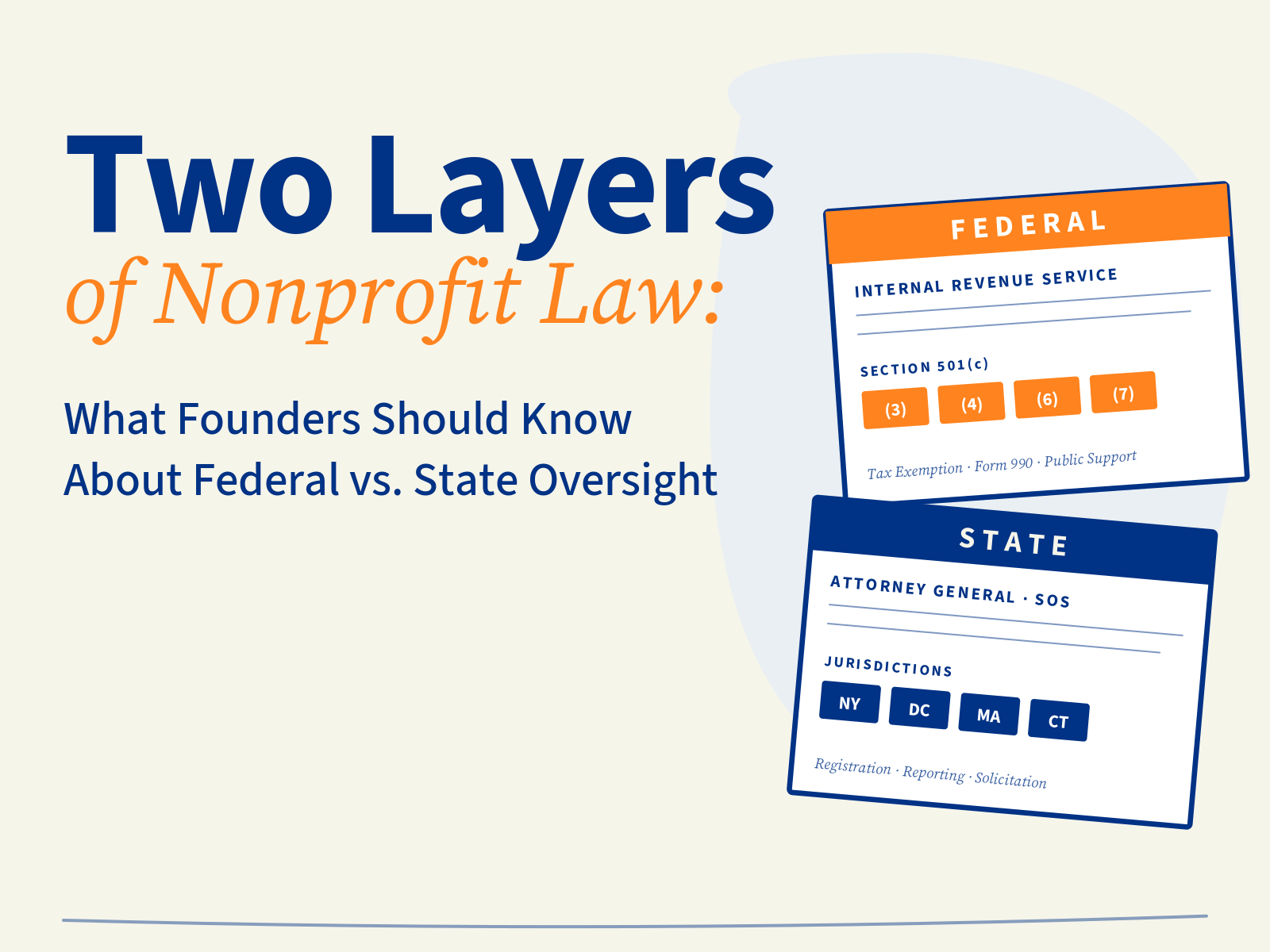

The Two Layers of Nonprofit Law: What Founders Should Know About Federal vs. State Oversight

Tax-exempt status is only half the picture: federal IRS rules and state nonprofit laws create distinct compliance regimes that sometimes conflict, and the cost of treating them as one stack falls hardest on the founders who didn't realize they had to file twice.

501(c)(3) vs. 501(c)(4) vs. 501(c)(6)

Most founders default to 501(c)(3) without realizing another subsection might better fit their advocacy ambitions, member-service model, or political reality, and here's how to pick the right one before you commit.

A Brief History: Part II

From the Revenue Act of 1917 to the Tax Reform Act of 1969 to today's Form 1023-EZ, the modern 501(c) regime is the product of a century of political compromise, and understanding why each layer was added is the fastest way to predict what regulators will look at next.

A Brief History: Part I

Modern nonprofit law didn't start with the Revenue Act of 1917; it traces back to the English Statute of Charitable Uses of 1601 and the common-law trust doctrine that still shapes how American courts interpret fiduciary duty today.

Three publications. One convenient monthly update.

Topical legal news from The Beacon. Resources from the Nonprofit Law Primer. Commonlight Legal news when it happens From the Hearth.

Ready to talk?

A complimentary 30-minute call with a managing partner. Clear scope.

Transparent fees. No primer required.